EXECUTIVE SUMMARY

For investors 2016 was a year of hope, while 2017 will be a year of delivery. One year ago, the consensus was that we had avoided another financial crisis but our expectations were modest, expecting a deflationary lower-for-longer environment. The pendulum has since made a full swing to euphoria and hopes of a panacea from Trump reflation. The truth is somewhere in the middle.

The global cyclical outlook has led to lower macro tail-risks. Many of the structural growth areas have already gone through a period of underperformance in light of the hope rally, making them relatively more attractive from the risk-return point of view. As these companies continue to deliver resilient earnings, we believe the market will return to fundamentals in 2017 and reward those that can deliver solid results.

KEY EVENTS & TRENDS

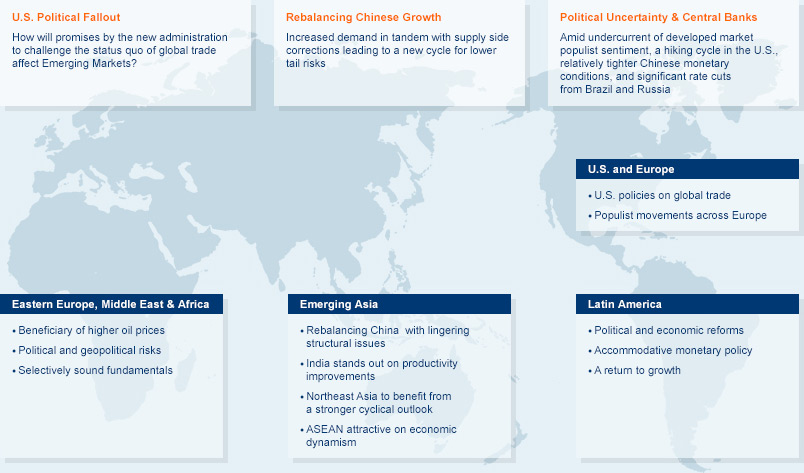

- US Political Fallout: In 2017, we will look to see the outcome and impact of the US’ new presidential administration, which could challenge the status quo of global trade and could also create a commodity demand surge in order to supply a massive infrastructure program.

- Rebalancing Chinese Growth: An upgraded global cyclical outlook from a higher growth contribution from the US affords China with a buffer to offset slower infrastructure over-investment with an export-led recovery.

- Political Uncertainty & Central Banks: 2017 will be marked by newly elected politicians pushing through their much-anticipated agendas along with actions from the world’s key central banks.

SEE ALSO

-

Mirae Asset LENS Issue 8 Part II FinTech: Reshaping Finance in Asia

Mirae Asset LENS Issue 8 Part II FinTech: Reshaping Finance in Asia -

Mirae Asset Brazil Macro Strategy Q&A with Andre Pimentel, Director of Investments in Mirae Asset Global Investments (Brazil)

Mirae Asset Brazil Macro Strategy Q&A with Andre Pimentel, Director of Investments in Mirae Asset Global Investments (Brazil) -

Mirae Asset LENS Issue 8 Part I Autonomous & Electric Vehicles: Smartphones on Wheels

Mirae Asset LENS Issue 8 Part I Autonomous & Electric Vehicles: Smartphones on Wheels -

Brazil’s Comeback Brazil has turned the corner and is, once again, presenting itself as an attractive investment opportunity.

Brazil’s Comeback Brazil has turned the corner and is, once again, presenting itself as an attractive investment opportunity. -

It’s not about Trump Rising dissatisfaction of the status-quo is not isolated and involves positives and negatives.

It’s not about Trump Rising dissatisfaction of the status-quo is not isolated and involves positives and negatives. -

Mirae Asset Global Fixed Income Strategy Q&A with Joon Hyuk Heo, Head of Global Fixed Income Investments.

Mirae Asset Global Fixed Income Strategy Q&A with Joon Hyuk Heo, Head of Global Fixed Income Investments. -

The Southeast's Glowing Archipelago The Philippines is an archipelago full of vigor and energy.

The Southeast's Glowing Archipelago The Philippines is an archipelago full of vigor and energy. -

India: Great Expectations India provides many reasons for investors to be bullish with exciting opportunities.

India: Great Expectations India provides many reasons for investors to be bullish with exciting opportunities. -

Demographics Support Wealth Creation in India Q&A with Neelesh Surana (CIO – Equity) of Mirae Asset Global Investments (India).

Demographics Support Wealth Creation in India Q&A with Neelesh Surana (CIO – Equity) of Mirae Asset Global Investments (India).