EXECUTIVE SUMMARY

We believe that emerging market (EM) equities are in the early stages of a multi-year recovery and are optimistic about continued EM outperformance vs. developed markets (DM) in 2018 and beyond. Looking to 2018, we are paying close attention to political continuity and economic stability in China, the start of a new global capital expenditure (capex) cycle, and attractive positioning and valuations for the EM equity asset class.

KEY EVENTS & TRENDS

-

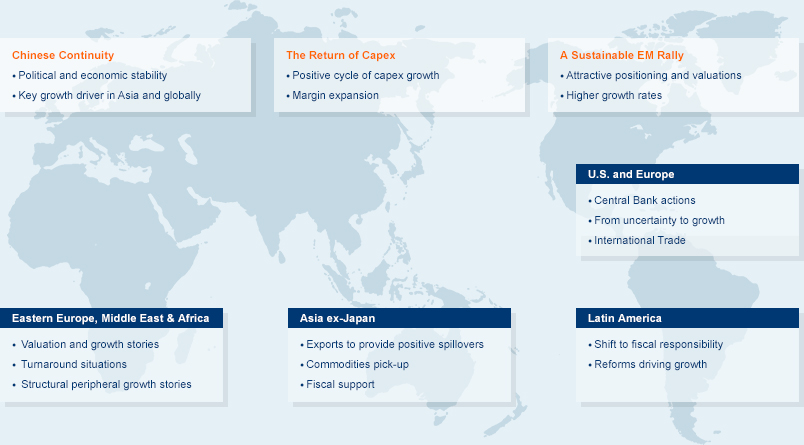

A Sustainable Rally in EM: We believe that EM equities are in the early stages of a multi-year run. Looking back to the mid-1970s, we have seen six EM bull cycles. On average, those cycles have lasted 42 months and delivered 228% returns in USD.1 As the current EM run has started less than 24 months ago and delivered only roughly a 45% USD return,2 we gain comfort with our thesis that EM equities still have a significant re-rating period ahead of them.

1. Bank of America Merrill Lynch, September 2017

2. Bloomberg, 11/30/2015-10/31/17 - Chinese Continuity: We maintain the view that China is not heading into a hard landing scenario and will continue to be a key growth driver for Asia and globally. China’s drive to deleverage will likely continue and should have a limited negative impact on growth. We expect the process to be gradual and policymakers will adjust accordingly if growth slows too much or if market conditions change.

- The Return of Capex: After almost half a decade of declining global corporate capex growth translating into negative demand for EM exporters, capex growth has pivoted back to a positive cycle. This change should help drive sustainable growth in 2018 and beyond as capex-led GDP growth tends to correlate with foreign inflows and a re-rating of asset prices.

SEE ALSO

-

Issue VI – North Korea Under the Radar Asia: Cutting Through the Noise Series

Issue VI – North Korea Under the Radar Asia: Cutting Through the Noise Series -

Compelling Opportunities in Emerging Markets Emerging market equities are delivering strong returns this year, extending their 2016 recovery

Compelling Opportunities in Emerging Markets Emerging market equities are delivering strong returns this year, extending their 2016 recovery -

Managing Indian Equities Opportunities and lessons from managing Indian equity investments for a decade

Managing Indian Equities Opportunities and lessons from managing Indian equity investments for a decade -

A New Era of Indian Fixed Income Q&A with Mahendra Jajoo (Head – Fixed Income) of Mirae Asset Global Investments (India)

A New Era of Indian Fixed Income Q&A with Mahendra Jajoo (Head – Fixed Income) of Mirae Asset Global Investments (India) -

Asia’s Clout in Global Biosimilars The biosimilar market remains in a nascent stage and Asian companies are increasingly competitive on the global stage.

Asia’s Clout in Global Biosimilars The biosimilar market remains in a nascent stage and Asian companies are increasingly competitive on the global stage. -

Case for an Unconstrained Bond Portfolio Infographic An emerging market bias in fixed income investing may offer attractive risk-reward opportunities.

Case for an Unconstrained Bond Portfolio Infographic An emerging market bias in fixed income investing may offer attractive risk-reward opportunities. -

New China: Impact of the Chinese Consumer Revisited New China continues to rapidly advance in the economy.

New China: Impact of the Chinese Consumer Revisited New China continues to rapidly advance in the economy. -

Asia’s New Middle Class Consumer The "sweet spot" of consumption resides in the upward mobility of the Asian middle class.

Asia’s New Middle Class Consumer The "sweet spot" of consumption resides in the upward mobility of the Asian middle class. -

Issue V – In with the New Consumers Asia: Cutting Through the Noise Series

Issue V – In with the New Consumers Asia: Cutting Through the Noise Series